EN

EN

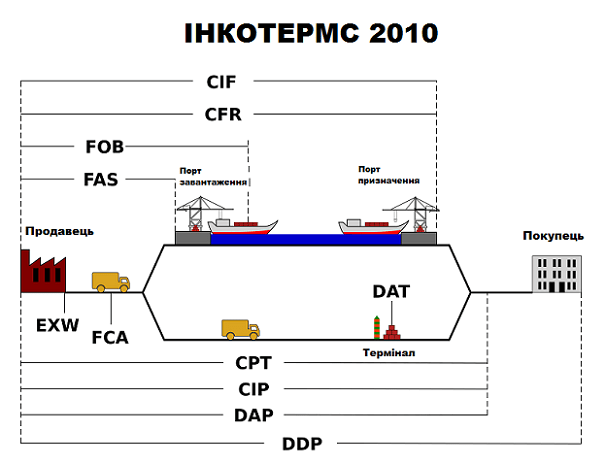

Incoterms 2010 (effective since 01.01.2011) is a set of international rules used in the global trade and recognized worldwide by government agencies, law firms, and merchants.

The scope of Incoterms 2010 covers the rights and obligations of the parties under the contract of sale in terms of the goods delivery.

What is the difference between Incoterms 2010 and the previous one, Incoterms 2000?

Incoterms 2010 provided for two new regulations, DAT and DAP, which can be used as multimodal. At the same time, 4 terms that were least used in practice were abolished, i.e. DAF, DES, DEQ and DDU.

*DAP – delivered at place, DAT – delivered at terminal.

• DAT replaces the term DEQ: the goods are provided to the buyer in unloaded form from the arriving vehicle.

• DAP replaces three terms – DAF, DES and DDU. It means that the seller has fulfilled his obligations when he has provided the buyer with the goods that are ready for unloading at the designated place.

Costs and risks on FOB, CFR and CIF delivery terms are redefined.

*FOB (free on board), CFR (cost and freight) and CIF (cost, insurance and freight).

According to the new Incoterms 2010, the transfer of risks is established after full shipment of cargo on board of the vessel.

Structure of Incoterms 2010 terms. Definition of abbreviations E, F, C, D

• Е – means that the seller has minimal obligations, limited to providing the goods at the disposal of the buyer;

• F – means that obligations are limited to sending the goods to the buyer when the main part of the delivery is not paid;

• С – means that the payment of the main part of the transportation shall be made in full. Responsibilities shall be transferred when the cargo arrives at the terminal;

• D – means the maximum scope of costs and risks vested on the seller. Obligations shall be transferred when the buyer has received the goods.

It is worth noting that the main obligations within the groups are somewhat different. For example, in group C (CIF and CIP) the seller must additionally insure the goods. In group D (DDP), he must pay import duties, and in groups F and D the differences are related to loading/unloading.

Incoterms 2010

Category E

Shipment

|

EXW |

any |

EX Works (… named place). |

Category F

The main transportation is not paid by the seller

|

FCA |

any vehicle |

Free Carrier (…named place) Transfer of |

|

FAS |

sea and |

Free Alongside Ship (… named port of shipment) |

|

FOB |

sea and |

Free On Board (… named port of shipment) Transfer of risks: From the moment of full loading on board of the vessel Export customs formalities: Seller’s responsibility |

Category C

The main transportation is paid by the seller

|

CFR |

sea and |

Cost and Freight (… named port of destination) Transfer of risks: From the moment of full loading on board of the vessel Export customs formalities: Seller’s responsibility |

|

CIF |

sea and |

Cost, Insurance and Freight (…named port of destination) Transfer of risks: From the moment of full loading on board of the vessel Export customs formalities: Seller’s responsibility |

|

CIP |

all vehicles |

Carriage and Insurance Paid To (… named place of destination) Transfer of risks: At the time of delivery/transfer to the carrier Export customs formalities: Seller’s responsibility |

|

CPT |

all vehicles |

Carriage Paid To (…named place of destination) Transfer of risks: At the time of delivery/transfer to the carrier Export customs formalities: Seller’s responsibility |

Category D

Delivery

|

DAT |

all vehicles |

new! |

|

DAP |

all vehicles |

new! Delivered At Piont (…named point of destination) Transfer of risks: At the time of delivery of the goods to the point specified by the buyer Export customs formalities: Seller’s responsibility Import customs formalities: Buyer’s responsibility |

|

DDP |

all vehicles |

Delivered Duty Paid (…named place of destination ) Transfer of risks: At the moment the goods are placed at the disposal of the buyer Export customs formalities: Seller’s responsibility Import customs formalities: Seller’s responsibility |

|

DDU |

all vehicles |

Excluded from Incoterms 2010 Delivered Duty Unpaid (… named place of destination) |

|

DAF |

all vehicles |

Excluded from Incoterms 2010 Delivered At Frontier (… named place) |

|

DEQ |

sea and inland waterway transportation |

Excluded from Incoterms 2010 Delivered Ex Quay (…named port of destination) |

|

DES |

sea and inland waterway transportation |

Excluded from Incoterms 2010 Delivered Ex Ship (… named port of destination) |

WHAT UKRAINIAN ENTREPRENEURS NEED TO KNOW ABOUT INCOTERMS 2010

When does Incoterms 2010 become effective?

Incoterms 2010 (International Commercial Terms) was published by the International Chamber of Commerce and has been widely used in international trade since January 1, 2011 along with the previous collections of rules, including the most popular Incoterms 1990 and Inco. Ukraine has a special situation with the entry of the updated version of the International Rules for the Interpretation of Commercial Terms into force.

Incoterms in Ukraine are certain rules prescribed by law, which will become mandatory in our country (for state regulatory and control authorities) 10 days after their publication in Uriadovyi Kurier. As of today, according to the Decree of the President of Ukraine on the Application of International Rules of Interpretation of Commercial Terms dated 04.10.94 N 567/94, the version of 2000 is mandatory. Application of the new Incoterms 2010 is not yet determined by applicable laws and they have not been translated into Ukrainian yet.

How to apply Incoterms 2010 during the customs clearance of goods

New delivery terms (DAT and DAP) in Incoterms 2010 have already been included in the Classifier of Delivery Terms used during the declaration of goods (Order of the State Customs Service of Ukraine dated 31.12.2010 N 1572). At the same time, the State Customs Service of Ukraine warns that the “Terms of delivery under DAT and DAP codes before the official publication of Incoterms 2010 cannot be used when concluding foreign economic agreements (contracts) under the law of Ukraine…”. This means that the use of Incoterms 2010 depends on the law applicable to the contract.

Rules for determining the law applicable to a foreign trade agreement

Article 6 of the Law on Foreign Economic Activity states that either the law chosen by the two parties to the contract or the law of the seller’s country should be applied.

It is worth noting that if the foreign economic agreement was withdrawn from the legal field of Ukraine, it is possible to rely on Incoterms 2010 and indicate new delivery codes in the customs declaration.

Should you worry about Incoterms 2010

It all depends on the conditions prescribed in your contract. If you refer to previous versions of Incoterms or do not use these rules at all, you can ignore the changes that come into force.

In case you do refer to Incoterms, please, note that since 01.01.2011 any reference to Incoterms in the contract signed on or after January 1 will mean a reference to Incoterms 2010 (unless, of course, the parties agree otherwise). So in this case it is required to think what amendments to make to comply with Incoterms 2010.

Thus, it is required to:

- check the existing contracts;

- made amendments, taking into account Incoterms 2010;

- make the required edits to the standard contract that will be used in the future.

The key amendments you need to know about

1. Four terms, DAF, DES, DEQ and DDU, disappeared and two new terms of delivery, DAP and DAT, were introduced.

2. Two classes of Incoterms were created:

- rules for any type of vehicles;

- rules for sea and river transportation (Incoterms 2000 had four classes).

3. The rules now apply to both international and domestic deliveries.

4. A reference to the use of electronic records has been introduced.

5. Insurance coverage has been revised taking into account amendments made to the Institute Cargo Paragraphs (Institute of London Insurers).

6. Clearly distributed costs at the terminal.

Why amending Incoterms 2010?

The decision to reduce the number of conditions was due to the fact that traders often chose incorrect or confusing conditions that lead to contradictory contracts. The new conditions do not depend on the chosen transport. When determining the customs value of goods delivered in accordance with the new terms, it should be taken into account that under the DAT terms, the cost of goods includes the cost of transportation to the terminal agreed by the parties and unloading at such terminal (excluding the insurance costs).

Under DAP, the invoice value includes only the cost of transportation to the place specified by the parties without unloading and insurance. The determination of the customs value of imported goods is facilitated by the fact that the new rules introduce the obligation of both parties to provide all required information upon request in cases of customs import-export clearance. The previous version of Incoterms did not oblige to such type of cooperation.

Source: “Customs Consultation”